Access to genetic information is becoming critical to the effectiveness of a new wave of medical treatments that are becoming available now. Personalized genetic services companies will act as a disruptive forces that are consumerizing genomic testing and driving rapid transformation of an industry that we expect to become a major force in personalized medicine. In this report, we consider how large this industry is likely to get in the next 10 years and start to evaluate how pharmaceutical companies, payers, providers and medtech companies will be impacted by the shift. We believe the emergence of ever cheaper testing technology means manufacturers can enhance clinical trials, payers can be selective in authorizing treatment payouts, and patients can have more confidence in outcomes.

1. A new industry is born

The introduction of relatively inexpensive biological assays, particularly around known genetic biomarkers and mutations, is creating a new industry. Today, personal genetic services companies such as 23andMe can provide inexpensive genetic analyses directly to consumers to help them understand their risk (or that of their pets) of several major genetic-based diseases. We are at the beginning of a new era in which assays and biomarkers are increasingly important in the treatment of cancers, degenerative diseases, and infectious diseases. The first Food and Drug Administration (FDA)-approved direct-to-consumer genetic testing service is 23andMe and, just as the iPhone release in 2007 changed the entire mobile phone market, we believe the FDA approvals received by 23andMe are creating a new market.

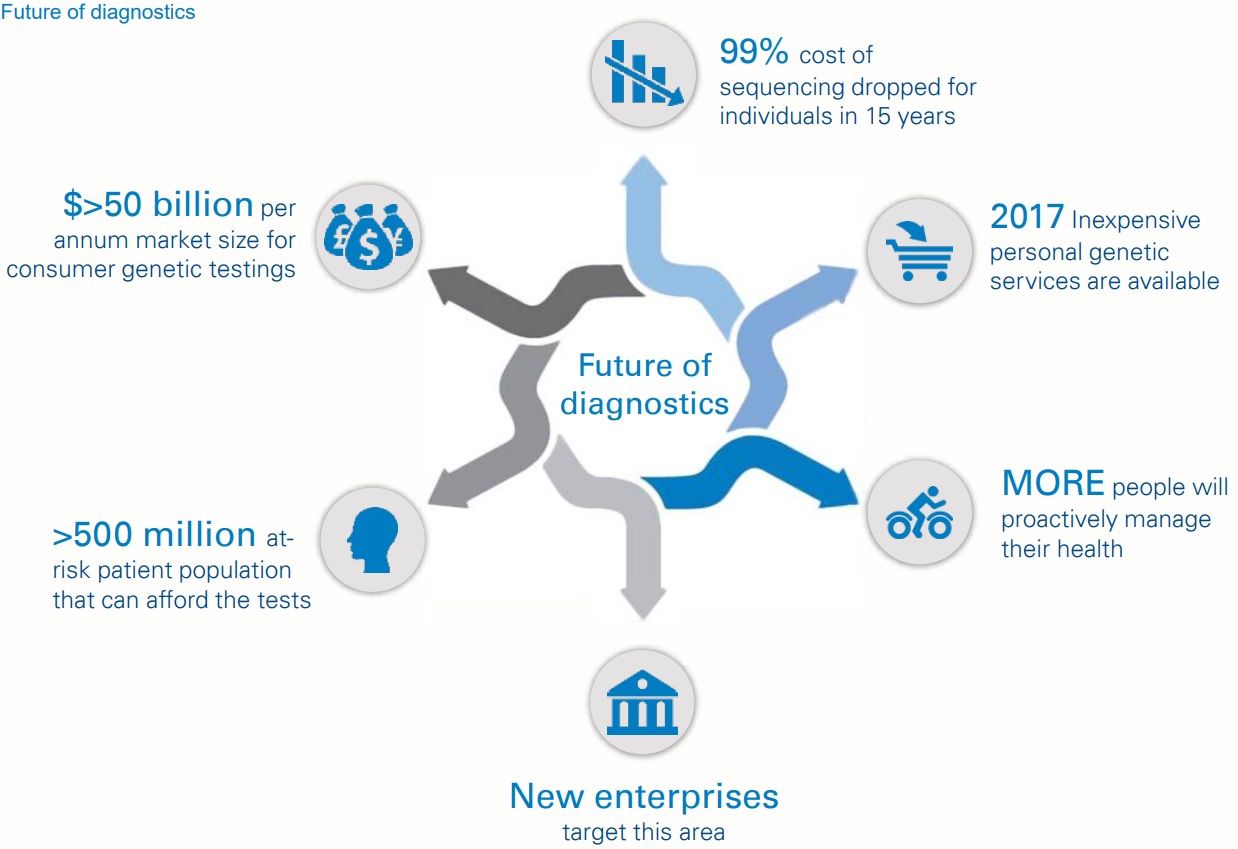

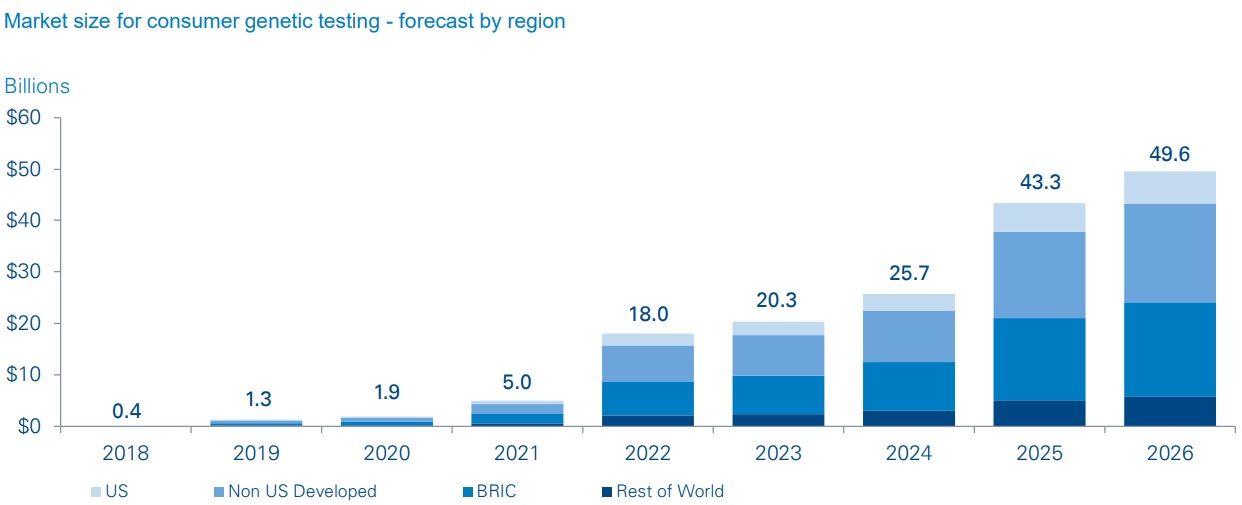

We expect the adoption curve of consumer-driven genetic testing to resemble that of other recent technology adoptions. In fact, there are many similarities between the introduction of smartphones and the breakthrough of consumer-based genetic testing. Prior to the release of the iPhone in 2007 there were, feature phones which provided email and allowed users to play simple games. In 10 years, we have seen growth which has led to 77 percent of the US population owning smartphones in 2017. A similar adoption curve makes it highly likely that the current small market for consumer genetic testing – similar to feature phones – has just undergone the same shift as the phone market did in 2007 and, in 2026, will be a $50 billion per annum business.

Why the huge growth? New, innovative treatments are very expensive, and often specific to genotypes or markers. Examples include the direct-acting antiviral therapies for the treatment of Hepatitis C, OPD1 inhibitors used to treat a variety of cancers, and chimeric antigen receptor T-cell therapy (CAR-T) for the treatment of certain childhood leukemia and B-cell malignancies. People suffering from these types of diseases, as well as those who want to understand and manage their personal risk of life-threatening diseases, have a better

understanding of their own genetic risk profiles and are much more engaged with the treatment profiles, than the general population. Today about 14 percent of the population has been identified as carrying a mutation or marker that puts them or their children at an increased risk of developing cancer, type-1 diabetes, cystic fibrosis, multiple sclerosis, arthritis, autism, Parkinson’s, or heart disease. In the developed markets alone, that includes over 240 million individuals. If we add in the BRIC (Brazil, Russia, India and China) and Middle East markets, which are developing fast in terms of buying power and adoption of advanced therapies, the at-risk patient population that can afford the tests is well over 500 million. If we add in individuals who test but do not have markers, the numbers become even larger.

To get approval for these very expensive treatments, pharmaceutical companies need to commit to the effectiveness of the treatment – for instance, Novartis has committed to not charging for pediatric treatment with the recently approved KymriahTM (CAR-T) therapy if there is no improvement in the first 30 days. This awareness of outcomes from treatments covers not just the manufacturer’s organizations, but the payer’s as well. The process needs to select the right patients, and those patients need to know if a treatment is going to work for them, as time is often is short supply. Every step of the way, from concept to new-drug investigation, to license, to reimbursement, to patient outcome, will be enhanced by the availability of diagnostic services that can reduce uncertainty and risk for the patient and align patient and supplier objectives. At the same time, developers of new therapies are delivering treatments based on greater understanding of genotypes, and patient populations are beginning to understand the risk profiles of certain genetic characteristics and mutations.

The demand for personal genetic services will grow rapidly as more people start using their genetic information to proactively manage their health. The traditional feature-phone analogy will no longer be sufficient for consumers; they will also need the iPhone of personal genetic services. Stakeholders that embrace this opportunity will find themselves in significantly enhanced competitive positions.

All stakeholders in the healthcare ecosystem stand to gain from the increasing availability and use of genetics-based diagnostics. Manufacturers can enhance their trials, payers can be selective in authorizing treatment payouts, and patients can be more confident of their outcomes.